Can I Gift Money From My Annuity To A Child And Avoid Tax Consequences?

Occasionally, we run into a client with an annuity contract they don't need. Cashing it out may cost them and keeping it isn't helping them, so they're considering giving that annuity to someone else. While this can be useful in some situations, the tax implications can be very real, and help from a knowledgeable advisor is recommended.

The Parties to an Annuity

There are several parties to an annuity and, usually, most of those parties are you. You have the owner, who is the person who bought the contract and the one receiving the payment. Next, you have the insured or annuitant. That's the person whose life is used to calculate the contract. Finally, you have the beneficiary. This is the person who receives the death benefit when the annuitant passes away.

When you give an annuity away, you're changing the owner of the contract, but you're not changing the annuitant. Your life is still the life that will trigger benefits and determine the amount. The new owner of the annuity can start receiving payments, change beneficiaries, and cash out the policy whenever they want.

To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust. There are some tax implications to consider with this, though.

Tax Implications of Giving Away an Annuity

Before you give an annuity away, you need to look at its status. Is it a qualified or non-qualified annuity? A qualified annuity is one that was paid for with pre-tax funds and was purchased for retirement. A non-qualified annuity is one purchased with after-tax funds and isn't necessarily a retirement vehicle, but it can be.

Your tax burden is going to change whether you purchased a qualified versus a non-qualified annuity. A qualified transfer can be more complicated than a non-qualified transfer if done incorrectly.

How to Transfer a Qualified Annuity

The issue with transferring a qualified annuity is the unpaid pre-tax dollars on the account. It should be noted that if you have qualified and non-qualified annuities, you cannot commingle them because they are taxed differently. There are two ways to transfer a qualified annuity:

- Cash out and repurchase. In this case, you would simply cash out the annuity and use the funds to purchase a new one. This is the least efficient way to do it because once you receive the funds, you're going to have to pay tax on them at an ordinary income tax rate.

- Custodian-to-custodian qualified transfer. In this case, the custodian (a.k.a. the insurance company) of the annuity would do a transfer to another custodian without the owner ever receiving a distribution of those funds. However, that does not mean it is a tax free transaction. The gifting of the qualified funds would need to follow rules under federal gift tax law. In addition, you would want to consult with your tax advisor regarding the income tax rules on qualified transfers. If the transfer is for charitable purposes, it is important to mention that as well.

Transferring a Non-Qualified Annuity

Transferring a non-qualified annuity is a bit simpler because these are purchased with after-tax dollars. In this case, all you have to do is fill out your insurance company's paperwork and have them manage the transfer on their end. This is a relatively seamless process that will require you and the individual receiving the annuity to agree to the transfer. Usually, it is often required that the signatures be witnessed and notarized.

Taxes can be due at the time of the transfer on any gains in excess of the original owner's cost basis on a non-qualified annuity. That means that there will be a tax burden to consider. Also, keep in mind that transferring a qualified or non-qualified annuity may impact your estate and gift taxes.

How the Transfer Impacts Your Estate and Heirs

Whenever you gift something to someone, if the overall value of the gift exceeds your annual gift tax exclusion of $14,000 per person per year, that is going to become part of the calculus under the unified estate and gift tax rules. So any gifting to an individual beyond the annual gift tax exclusion limit reduces the remaining exemption for estate and gift tax.

One of the reasons people consider transferring an annuity is because they want to avoid paying the eventual estate taxes created by owning it. Transferring an annuity will remove that concern from your estate in most cases. However, there is an exception to this. That's called the three-year rule.

How the Three-Year Rule Impacts Your Transfer

If you die within three years of giving that annuity away, whether you give it to a trust or a person, the value of that annuity will be added back into your estate. As many people are getting rid of their annuities to reduce their estate size, that three-year rule defeats the purpose for giving an annuity away.

This three-year rule doesn't just apply to annuities. It applies to any transfer you make of an asset when the transfer isn't made for comparable consideration. Comparable consideration means that if the individual doesn't pay reasonable value for the item, it's considered a gift. So you can't, for example, sell your entire annuity to a relative for $1 to get around transfer rules. However, if you were to sell the annuity outright to a company that buys annuities, that would not be considered a transfer and the three-year rule wouldn't apply.

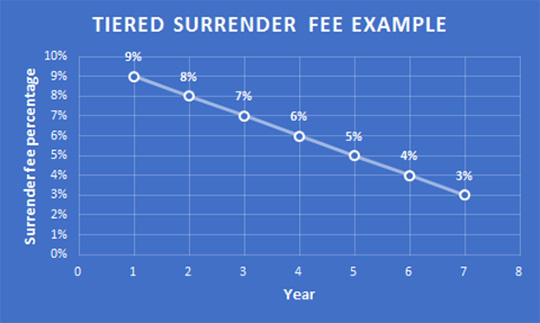

Finally, note that none of these transfer rules eliminate the surrender fees associated with early termination of an annuity. If you choose to move the annuity to another carrier for example, under the new owner, surrender fees may still apply. Internal changes of ownership will not, generally, create new fees. When they do apply, surrender fees are usually charged at a tiered level over a set period to time. The percentage you'll pay to surrender an annuity will be higher in the first years of your contract than toward the end. The chart below shows an example of how surrender fees would decrease over time.

Often, when you try to get out of an annuity, you're going to deal with fees and tax implications. Changing ownership with the same carrier can be a viable option for avoiding these fees. Surrendering an annuity for a new annuity with a different carrier in the name of the new owner will often entail surrender charges since it would not qualify as a 1035 exchange since that requires identical ownership. That's why we recommend consulting with a true annuity professional before proceeding.

Exchanging the Annuity to Eliminate Taxes

The IRS allows you to exchange an out-of-date non-qualified contract for a more recent contract that may be more suitable. Under a 1035 exchange, you can replace that old annuity for a better one, without having to pay taxes on any gain in the policy provided you follow the 1035 exchange rules.

If someone wanted to provide for heirs using an annuity, we would recommend making them the beneficiary of the annuity in the event of your death, rather than giving it to them outright. This is because the annuitant can then expand the payments and create a stream of income based on their lifetime. Here's how the scenario works:

- You trade an old, underperforming non-qualified annuity for a new one under a 1035 exchange.

- As the annuity is non-qualified, no required minimum distributions are due. As such, you allow the annuity to continue accumulating value until you pass away.

- On your death, the beneficiary can elect to become the new owner of the annuity and can receive payments based on their own lifespan.

This process allows one annuity to last several lifetimes by using a "stretch" provision. Stretch provisions can be complex and vary by carrier and type of asset. It is important to be sure that the insurance company you are using or are considering can accommodate your "stretch" goals.

Another benefit to the 1035 exchange is that in some rare cases, the insurance companies will waive any surrender charges made as part of one of these qualified transfers provided the annuity remains with the same insurance company. However, if you want your annuity to benefit your heirs now, and a 1035 exchange is not the answer, you may consider transferring it to a trust. Just be aware of fees and tax considerations.

Transferring an Annuity to a Trust

An irrevocable trust is an often-used tool for removing assets from your estate while providing for beneficiaries. The process of transferring an annuity to a trust may be a bit more complex. This is because you're going to want to make the trust the owner and beneficiary of the annuity. The trust would then dole out funds according to its preset terms. In addition, the type of trust you transfer the annuity to determines the possible tax consequences.

However, the trust can't be the annuitant for one simple reason: Trusts don't have life expectancies. In essence, if the trust was the annuitant, then the annuity would have to pay out forever. The annuitant/insured is the individual who the life expectancy is based on. Generally, annuities pay more if the insured is older. When you make the trust the owner and beneficiary, it is going to receive payments based on your life expectancy. Those payments are then used to fund the trust.

In a way, it's similar to an irrevocable life insurance trust (ILIT) but with one major change. While an ILIT doesn't receive the bulk of its funds until the life insurance contracts are paid out after your death, the annuity will pay out only while you're alive and will stop paying when you pass away. If the trust is also the beneficiary, it will receive the death benefit. If you list a relative as a beneficiary, the death benefit on the annuity will be paid out directly to them.

It's important to note that to avoid any estate tax implications, that trust needs to follow the same standard rules to preserve its estate tax shelter status. That means:

- It must be irrevocable. An irrevocable trust means that you have no control over it once you transfer funds into it.

- It must be set up for the benefit of a living person. This is required for it be considered a tax shelter trust. Beneficiaries can't be businesses or even future interest for heirs not born yet.

- You must have no ownership interest. The IRS considers you to have an ownership interest in a trust if you have any rights to make changes to the trust. That means you can't set yourself up as the trustee or make benefits payable to your estate. In addition, your spouse should not act as a trustee because you and your spouse are considered one legal entity for tax purposes.

- Beneficiaries must be able to access funds. This is an odd provision, but it's one designed to prevent you from accidentally making your trust invalid. To be an estate tax shelter, a trust has to be set up for someone's current interest. This is something called Crummey provisions. It means that the trust will have to send out notifications every time it receives a payment on behalf of the beneficiary, letting the beneficiary know that they have funds available that they are free to remove.

Decisions about using a trust with your annuity will depend on your situation. An annuity without an irrevocable trust is likely a lower-cost option, but this could impact your estate taxes. The trust can be used to fund a larger amount of money with no estate tax implications, but it doesn't allow you as much control over those funds once they're in the trust. Sometimes, teaming them together can create the most impact.

Often, a much better idea than all of this is to simply take a taxable distribution and, after netting out the taxes, use the distribution to pay an annual premium on a survivorship life insurance policy, or individual policy if you are single or have a spouse in poor health. This will secure you a very large tax-free death benefit for your heirs or favorite charity.

In this manner, you avoid the major concerns of transferring ownership to leverage the income from the annuity into a tax-free death benefit valued at many times the value of the annuity. As an example, we recently met with a couple, ages 70 and 69, who will be taking their after-tax annuity proceeds of $80,000 annually to purchase a $5 million survivorship policy that would be equivalent to $10 million given the net worth and tax status of that couple.

If the couple dies early, the heirs receive the value of the annuity and the life insurance proceeds as well. It would be near impossible for a couple that age to convert $80,000 a year in any traditional risk-bearing investment to a $10 million equivalent during their lifetime. Talk about creating wealth!

There are many considerations, and it's often a hard decision to make. However, it is the type of decision we think about in-depth whenever someone is considering transferring an annuity to someone else. In some cases, it may work, while in others, there's a more tax-friendly alternative. For more information on providing income to heirs, contact a Howard Kaye advisor at 800-DIE-RICH.

FREE: Learn How Our Clients Discount Their Estate Taxes By Up To 90% (We Created This Technique)

Can I Gift Money From My Annuity To A Child And Avoid Tax Consequences?

Source: https://howardkayeinsurance.com/the-ultimate-guide-to-transferring-annuities-as-tax-efficiently-as-possible/

Posted by: ledfordsholebabluch.blogspot.com

0 Response to "Can I Gift Money From My Annuity To A Child And Avoid Tax Consequences?"

Post a Comment